But even that's subjective. If home ownership were considered essential, we'd say there's high inflation. The only unquestionably high inflation is Weimar-style. Everything in the middle is justifiable in either direction, and gray matters seem subject to whichever ways the political winds blow. If it's convenient for rates to stay low, they will.

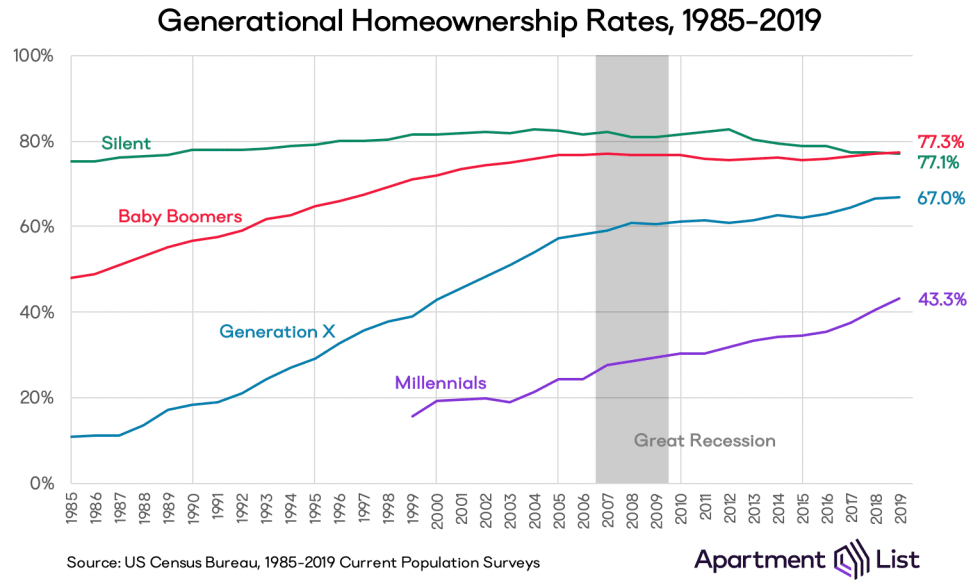

Correct, and housing services do not mean ownership. Inflation metrics say a 700 square foot econobox is the appropriate measure of cost. If you continually shift the basket, then you can craft whatever CPI number you're looking to achieve. And ownership levels by generation aren't what they used to be:

Sure. But that's not inflation. That's an increase in housing prices. If housing prices rise but rents do not, it doesn't make a difference to consumption - your consumption is either the rent you pay or the imputed rent. If buyers want to bid up the price of housing past what renting it out will pay for, that's their problem.

And at the risk of just reposting this comment on HN all the time. Focusing on central banks as the driver of asset price increases is looking in entirely the wrong direction. There is a third component that pushes both asset prices and central bank policy - the global supply/demand of savings vs investment opportunities. Which is driven mostly by demographics. China's massive working class, and the unprecedented rate at which they are getting wealthier, and their savings rate which is like >10x the average US citizen means there is a huge increase in the global supply of savings. Which bids up asset prices and pushes down yields, as savers compete with each other to buy up the extant profitable and safe opportunities. Central banks are the on the receiving end of this too: over-saving pushes down the natural rate of interest, which means policy rates must be lower to respond (unless you want to condemn some working Americans to unemployment). So long-term interest rates fall, and central banks have less operating space to smooth out the business cycle by moving short-term rates.

The U.S. Bureau of Labor Statistics reports (10-Feb-2021) that the Consumer Price Index (all items index) increased 1.4 percent over the last 12 months.

That's not "nearly everything". Most people don't spend their salaries on lumber or copper. If anything, it shows how little the prices of raw commodities affect consumer prices.

It's also hardly evidence for impending hyperinflation. For instance, aluminum is massively cheaper than in 2008, and copper is still quite a bit below the 2011 level. Commodity prices always fluctuate massively.

Corn is much lower than it was 8 years ago, steel is at the same level as it was in 2018/2019, lumber only up 50% from last peak in 2018 (and price fluctuates a lot currently).

{kind=link}

Except for the part where the fed said (and continues to say) it would raise rates if it saw sustained high inflation